Paris is one of the deepest M&A markets in Europe, and it runs on rules that nobody writes down in English. Most of the advice students read is London advice, and London advice fails in Paris at three exact points: the internship system, the school hierarchy, and the CV itself.

I broke into Paris M&A from SKEMA, not from HEC, and finished my banking career as an Executive Director. So when I describe the hierarchy below, I am describing a wall I climbed, not a wall I guard. Here is how the market actually works.

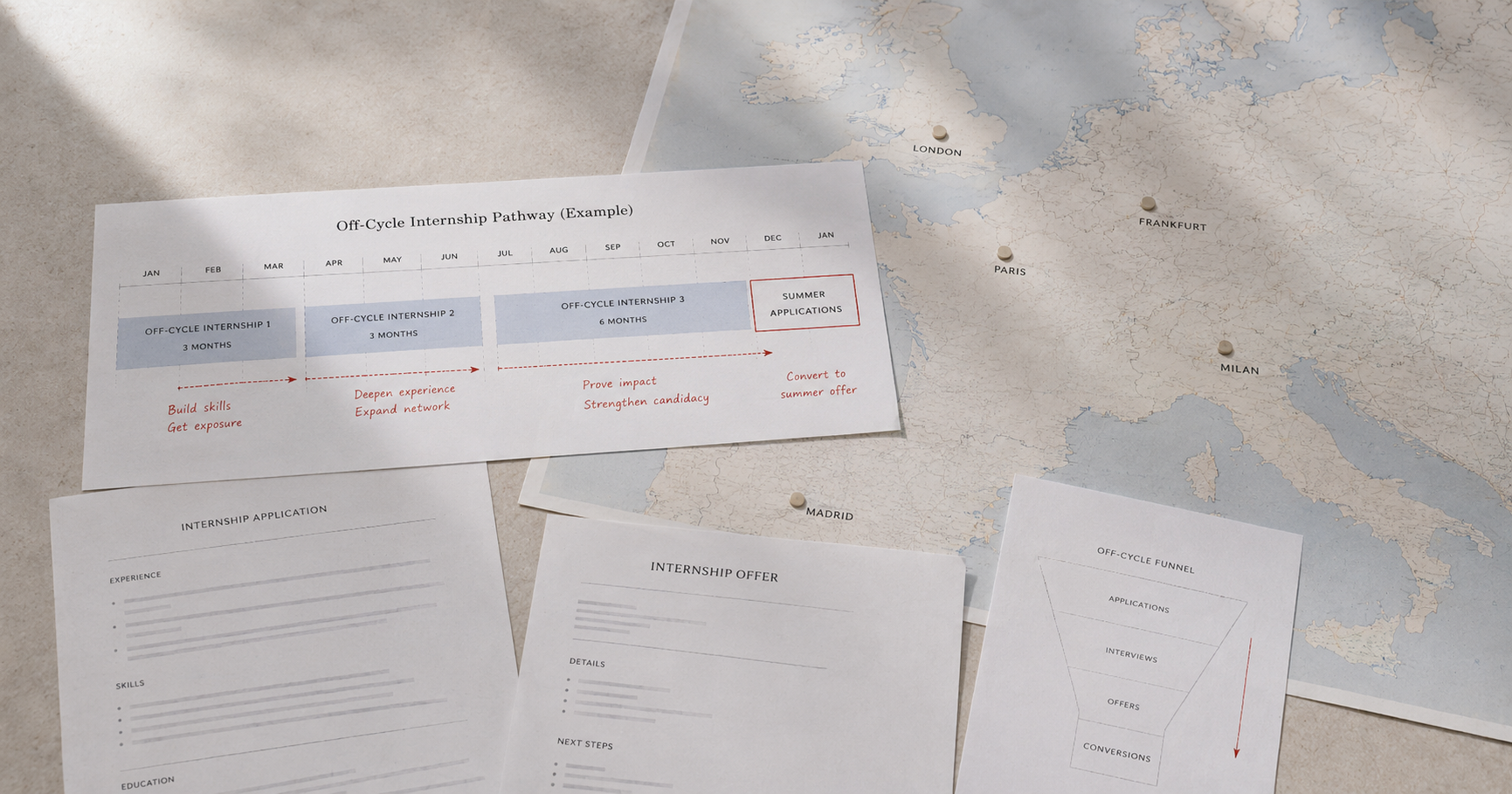

The currency of Paris recruiting is the stage, not the summer

London recruiting revolves around the ten-week summer internship. Paris revolves around the stage: a six-month internship where you are staffed like a junior analyst, on live work, for long enough that the team genuinely knows what you are by the end. The global banks run summer programmes in Paris too, but the volume of seats and the real conversion path run through stages.

Hiring is close to continuous. January and July intakes dominate, applications open on a rolling basis roughly three to six months before each start date, and the market treats your stage count as the spine of your CV. A serious Paris candidate arrives at graduation with two or three M&A-relevant stages already banked. That is the bar you are competing against, wherever you come from.

The césure system, explained for outsiders

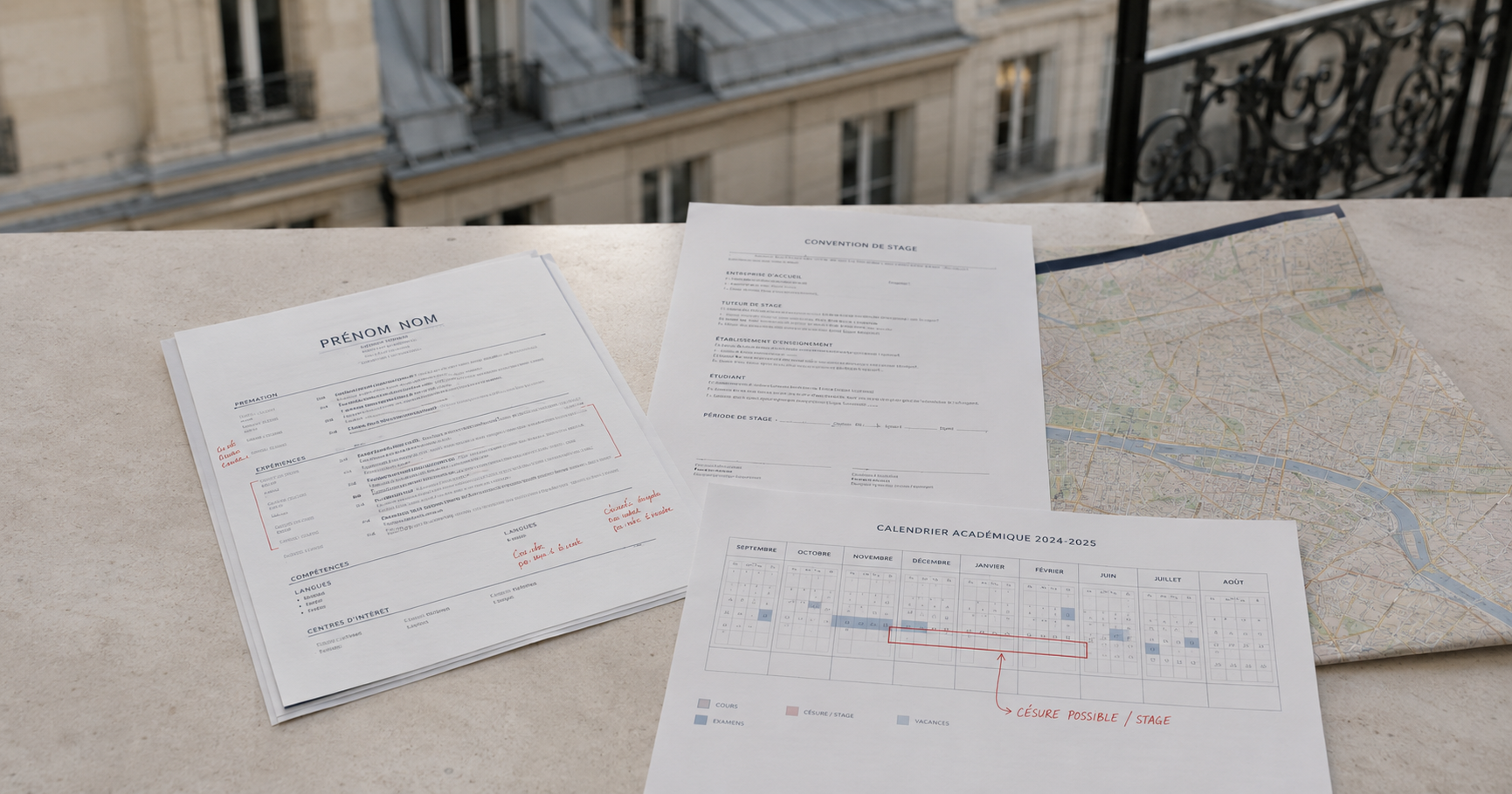

The reason French candidates arrive with so much experience is structural. Most masters students take a césure: a sanctioned gap year between the first and second year of the masters, designed precisely to stack two six-month stages. After the césure comes the final year, and then the stage de fin d'études, which is very often the seat that converts to the full-time offer.

Two implications. If you are French, the sequencing decision matters more than the first logo: use the first stage to get reps anywhere credible (a good boutique teaches you more, faster, than a big platform where you are the fifth intern), then spend the second stage on the brand and the conversion play. If you are not French, understand that your competition has twelve to eighteen months of deal experience before their first full-time interview. Plan your own experience accordingly rather than resenting the maths.

One hard constraint for non-enrolled candidates: a classic stage legally requires a convention de stage, a tripartite agreement with an educational institution. If you are not enrolled somewhere that can issue one, you cannot do a stage in the standard form; the routes around it are enrolling in a programme, or targeting the contract-based and off-cycle style roles that international firms run. Verify the current rules, but do not discover this constraint at offer stage.

The school hierarchy, honestly

It is real, it is steep, and pretending otherwise wastes your time. HEC, ESSEC and ESCP sit at the top of the business school ladder; the elite engineering schools (Polytechnique and its peers) run their own respected lane; a second circle follows, and then everyone else. Paris screens weight the school line more heavily than London does. That is the uncomfortable truth, and you should plan around it rather than argue with it.

Here is the part the fatalists miss: the hierarchy sets the default, not the outcome. Three things move candidates across circles, and I used all three. First, the stage record: after your first real M&A stage, the experience line starts to outweigh the insignia, and it compounds with every seat. Second, networking: alumni where you have them, and thinner threads where you do not (same city of origin, same society, same first employer). Third, technical over-preparation, because Paris gives you the arena for it.

The Paris interview: harder technicals, colder rooms

Expect more technical depth than the equivalent London first round. Accounting mechanics pushed further, valuation bridges done aloud, mental arithmetic without apology, and at some houses the occasional brainteaser. Fit is tested, but the process is drier and more proof-led than story-led; charm buys less here than anywhere else I worked. For a well-prepared candidate this is good news: the Paris interview rewards exactly the preparation that weaker candidates skip.

On language: domestic French M&A works in French, with English documents. For most coverage seats, fluent French is effectively required. The exceptions are the international teams and the cross-border platforms; if your French is not there, target those deliberately or enter the platform through London first.

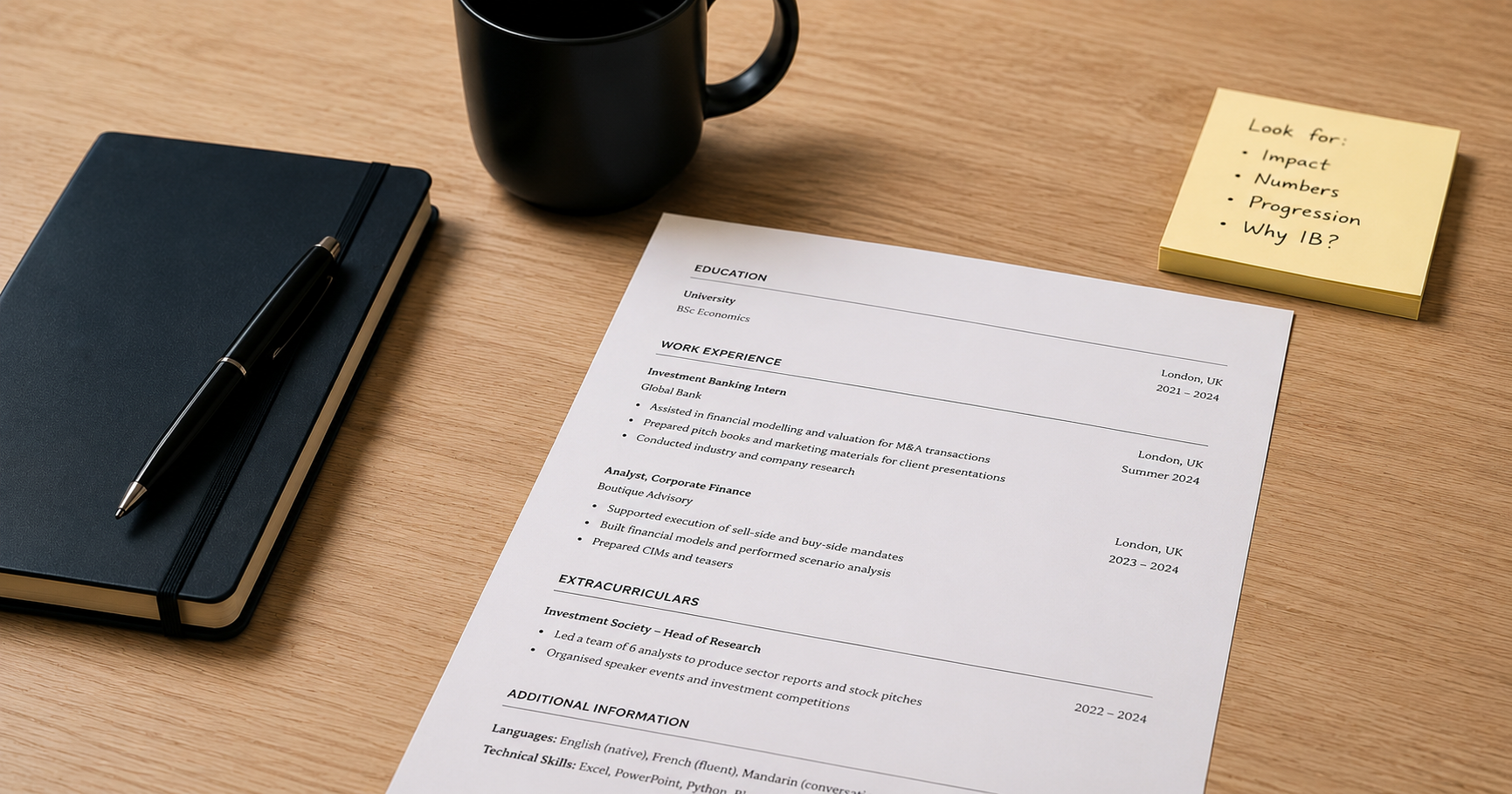

The French CV

The standard is the same one every serious market uses: one page, achievement bullets built on verbs and numbers, dates aligned, zero typos. The local differences sit at the edges. A photo was long the French convention; it is now optional and declining, and for any English-language application, and anything that touches London, remove it entirely. Keep two versions of your CV if you are running both markets.

Show a mention bien or better, show a strong rank, and if you did a prépa, keep the line: it means something to a French reader that it does not mean elsewhere. Beyond that, the disease is the same as everywhere: responsibilities instead of achievements. A stage described as “participation aux missions de l'équipe” is a stage wasted twice.

A route map by profile

- Grande école student: run the system as designed. Applications for césure stages go out four to six months ahead; boutique first for reps, brand second for conversion; then make the stage de fin d'études count.

- Non-French candidate targeting Paris: run an honest French language check before anything else. Target international teams, consider entering via London or an off-cycle seat, and solve the convention de stage question early.

- French student outside the top circle: my route. Thinner-thread networking, earlier and more stages than the default calendar, and technical preparation past the point that feels reasonable. It works. It simply costs more effort than the HEC route, and the sooner you accept the pricing, the sooner it starts paying.

FAQ

Do I need to speak French for M&A in Paris?

For domestic coverage, effectively yes. International teams and cross-border platforms are the exceptions; target them deliberately.

Is a photo required on a French CV?

No longer required, still seen. For English-language applications, remove it. If applying in French, follow the convention of the firm you are writing to.

Can I do a stage if I am not enrolled in a French school?

Not in the classic form: a stage requires a convention de stage from an educational institution. The workarounds are enrolment, or contract-based and off-cycle roles at international firms. Check the current rules before building a plan on either.

How many stages do converting candidates typically have?

Two or three M&A-relevant seats is the norm among candidates who convert to full-time in Paris. Plan backwards from that number.

The outreach system that opens these doors, from alumni to thinner threads to the referral itself, is in the IBD Networking Playbook.

Get the free Networking Playbook

Former Executive Director in TMT Investment Banking at Nomura and M&A banker at BNP Paribas. Top-rated Head Mentor on Wall Street Oasis with 300+ sessions. About