Every bank has the same org chart and almost nobody explains it to candidates before they are asked to choose a seat on it. One axis is industries: TMT, FIG, healthcare, industrials, consumer, natural resources. The other is products: M&A, leveraged finance, equity capital markets, debt capital markets, restructuring. Where those two axes cross is where you will actually sit, and the choice shapes what you learn, the hours you keep and the doors that open two years later.

I spent fifteen years on both sides of the divide, product first in M&A at BNP Paribas in Paris and London, then coverage as an Executive Director in TMT at Nomura in Hong Kong. So this is not a neutral explainer. It is a comparison from someone who has done both jobs and hired for both.

What each seat actually is

An industry group, also called coverage or a sector team, owns the client relationship. The TMT team knows every software company, telecom operator and chip maker in its region, calls on them constantly, and brings them ideas: an acquisition, a disposal, a listing, a refinancing. When one of those ideas becomes live, coverage either executes it or pulls in the relevant product team.

A product group owns one type of transaction and runs it across every industry. The M&A team executes mergers whether the client makes semiconductors or shampoo. Leveraged finance structures debt for sponsor buyouts. ECM runs IPOs and share placements, DCM runs bond issuance, restructuring handles companies in distress. Product bankers are specialists in a craft; coverage bankers are specialists in a client base.

How much this division matters varies by bank and region. Some American firms push M&A execution into the sector teams, so a TMT analyst there models mergers directly. Many European banks keep a central M&A group and country coverage teams. In Asia, coverage is king: relationships drive everything, and product often sits at the regional hub serving several markets at once. Ask how the specific bank splits the work, because the same group name can mean two different jobs at two different firms.

What you learn in each, said plainly

- Coverage teaches breadth and commercial judgement. You see every product type touch your sector: a merger this quarter, a convertible next, an IPO after that. You learn how companies in one industry are valued, what their CEOs worry about, and how business actually gets won. The cost is that in a marketing-heavy team you can spend long stretches on pitch decks rather than live deals.

- M&A teaches execution density. Deal after deal, you build models, run processes, draft the documents that move money. It is the closest thing banking has to a technical apprenticeship, and it is why buy-side recruiters treat the M&A stamp as a proxy for training. The cost is narrowness: you may know everything about process and little about any one industry.

- ECM and DCM teach markets. You live on pricing, windows, investor demand. The hours follow the market more than the deal, which usually means earlier nights and real weekends. The trade is less modelling: a DCM analyst can go a year without building a full operating model, and exit interviewers know it.

- Leveraged finance sits in between. Credit analysis, sponsor clients, real modelling. In banks where LevFin runs the model rather than just the financing grid, it is one of the best trained seats in the building and private equity firms treat it accordingly.

- Restructuring is the countercyclical craft. Busiest when everything else is quiet, technically dense, and a small world where reputations form fast.

Hours, and who gets paid

The folklore says product works harder than coverage. The truth is that live deals work harder than marketing, wherever they sit. A coverage team with three live mandates is a harder seat than a quiet M&A group. Directionally, though: M&A and LevFin carry the heaviest and least predictable load, capital markets the most civilised, and coverage swings with the deal pipeline. Pay at analyst level is set by the bank, not the group, so the real compensation difference is your bonus bucket and, over time, which groups generate revenue. If you want the full ladder, I have set out the numbers from analyst to MD separately.

The exit question, since you are asking anyway

Private equity funds hire modelling reps and deal reps. That favours M&A, leveraged finance and any coverage seat that executes its own transactions. A sector seat also carries a second advantage people underrate: sector funds hire sector bankers. A TMT analyst is a natural candidate for a technology fund; a FIG analyst for a financials specialist. The narrowest exits sit in DCM, which is a genuinely good job that maps to fewer buy-side seats. I have written an honest map of the exits if that is the deciding factor for you.

How to actually choose

Most banks decide placement through some mix of preference lists, interviews with the groups and internal networking. Treat it as a second recruiting process, because it is one. Three rules from the hiring side.

- Choose deal flow over prestige. The busiest group at a decent bank trains you better than a sleepy group at a famous one. Ask juniors how many live mandates they personally worked in the last six months, and listen to the pause before the answer.

- Choose people you can survive. You will spend more waking hours with your staffer than with anyone you love. A brutal culture in a prestigious group breaks more careers than a modest group ever stalled.

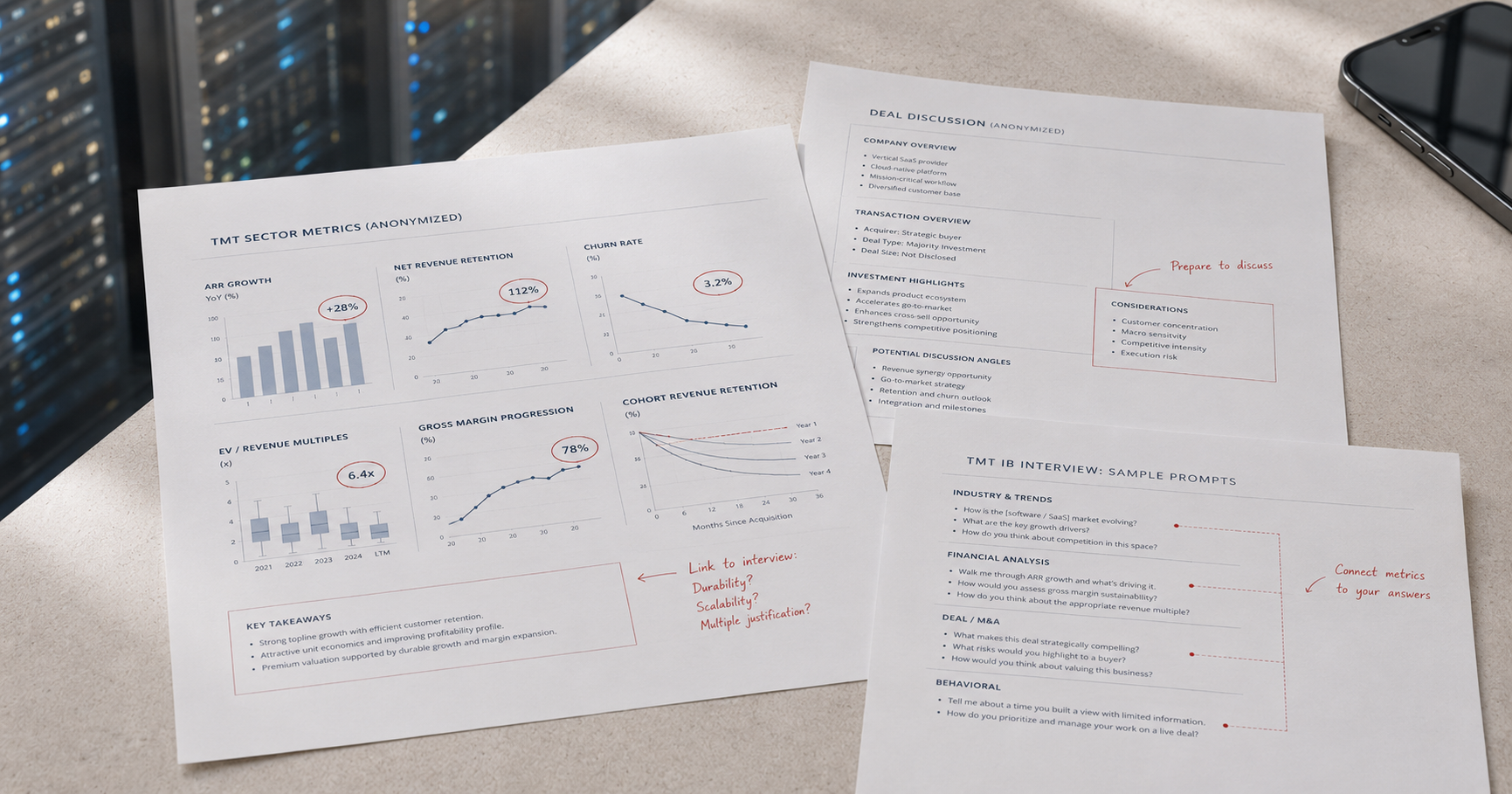

- If you have a sector story, use it. A genuine interest in one industry, evidenced on your CV, is worth more in a coverage interview than a generic strong profile. If TMT is that sector, I have written about what its interviews actually test.

FAQ

Can I move from a product group to coverage later, or the reverse?

Yes, and it is easier inside the same bank than across banks. Internal mobility after 18-24 months is normal where you have a sponsor. The clean moves are product to coverage in the same sector you served, or coverage to the product you used most.

Is ECM or DCM less prestigious than M&A?

Prestige is the wrong lens. Capital markets are excellent jobs with better hours and narrower exits. If you want the buy side, weight M&A or LevFin. If you want banking as a career with a life attached, capital markets are underrated.

Does group matter more than bank?

Within a tier, yes. A top group at a solid bank beats a weak group at a famous one for training and exits. Across tiers the calculation changes, and I would take the platform question seriously before the group question.

If you are holding an offer and trying to read the groups from the outside, that is exactly the kind of decision the IBD Recruiting Review exists for: one hour, one to one, with someone who has sat in the seats you are choosing between.

Book the 60-min IBD ReviewView Full Cycle

Former Executive Director in TMT Investment Banking at Nomura and M&A banker at BNP Paribas. Top-rated Head Mentor on Wall Street Oasis with 300+ sessions. About