Tell me about a deal that interested you recently. The question appears in nearly every serious IBD interview, and it quietly separates candidates into two groups: those who read headlines and those who think like advisers. I asked it for years at Nomura and BNP Paribas, and the pattern never changed. Weak answers narrate. Strong answers argue. The difference is structure, and structure can be learned in an afternoon.

Choosing the right deal

The hierarchy is simple. A deal you personally worked on beats everything. A recent deal done by the bank interviewing you comes second, because it shows targeted preparation and lets the interviewer add colour. A well-chosen market deal comes third and is completely acceptable, provided it is recent, relevant to the group, and small enough in fame that you are not reciting the same answer as the previous four candidates. Pick something announced in the last 6-12 months, in or near the sector you are interviewing for, and ideally with a feature worth discussing: an unusual structure, a contested premium, a strategic surprise.

One deal prepared deeply beats three prepared thinly. You need to survive five minutes of follow-ups, not deliver one minute of summary.

The five-part structure

- Headline. One sentence: buyer, target, size, deal type. This proves control before anything else.

- Terms. Price, premium, consideration, anything structurally interesting. Two or three precise facts, not a data dump.

- Rationale. Why the buyer did it, in 2-3 catalysts with a proof point each. This is where narration becomes argument.

- Valuation logic. How the price can be justified and what the buyer is underwriting. You do not need a model; you need the drivers.

- Risks and your view. One or two specific risks, then a two-sentence opinion. The opinion is what most candidates omit, and it is the part interviewers remember.

The worked example: 3G Capital takes Skechers private

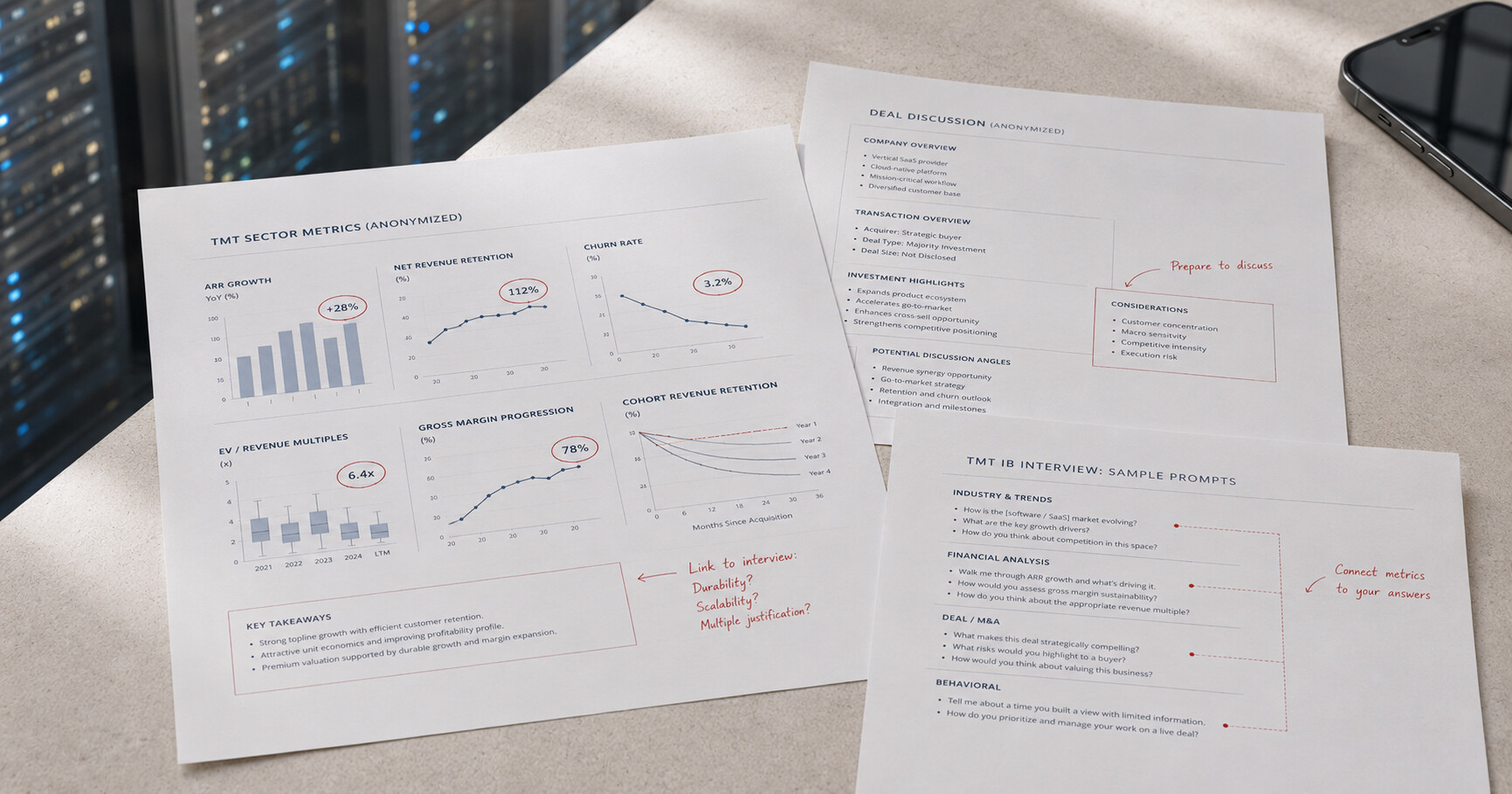

Headline: in 2025, 3G Capital completed the take-private of Skechers, the global footwear brand, at an equity value of roughly US$9.4bn.

Terms: shareholders were offered US$63.00 per share in cash, a premium of about 28% to the unaffected close of US$49.37, or alternatively US$57.00 in cash plus one unlisted equity unit in the new private parent, with that election capped at 20% of shares. Announced 5 May 2025, closed 12 September 2025, at which point the shares stopped trading.

Rationale, three catalysts. First, scale and stability: Skechers is the world's third-largest footwear brand, with 2024 revenue of US$8.97bn and net earnings around US$640m, the kind of steady compounder that suits private ownership. Second, diversification: roughly 62% of sales were international and sourcing was spread across Asia rather than concentrated in one country, which softens tariff and supply risk. Third, the operational angle: 3G's playbook is cost discipline, and Skechers offered margin upside in procurement, inventory and the growing direct-to-consumer mix, already 43% of sales, without needing to replace management, since the founding Greenberg family stayed on.

Valuation logic: the 28% premium is a control premium plus the value of executing improvements away from quarterly scrutiny. The buyer is underwriting durable revenue, margin expansion and the DTC shift. A sanity check without a model: triangulate the implied multiple against footwear comparables and ask whether plausible efficiency gains earn back the premium.

Risks and view: the thesis breaks if cost discipline damages the brand, or if a consumer slowdown forces markdowns. My view in an interview: the deal makes sense because the operational upside fits the buyer's playbook and leadership continuity lowers execution risk; the swing factor is cutting cost without cutting momentum. Two sentences, position taken, done.

The follow-up traps

- Is the premium fair? Never answer yes or no alone. Fair if the underwritten improvements are achievable; aggressive if they are not. Name the improvements.

- How would you value it? Give the toolkit in one breath: trading comps, precedent transactions, a DCF, and for a sponsor deal the LBO maths of what returns the price implies. If the conversation goes deeper, you are into the territory I cover in how modelling tests are actually scored.

- What would kill the deal? Regulatory conditions, financing certainty, shareholder approval. For a non-horizontal take-private like this one, approvals and process mechanics matter more than antitrust overlap.

- Numbers you do not have. Say not disclosed, then reason directionally. An invented number discovered in follow-up ends the interview; a structured directional answer strengthens it.

- Would you have advised the seller to accept? Flip to the other mandate's logic: certainty of cash at a 28% premium against standalone upside and market risk. Arguing both sides of the table in one answer is the fastest way to sound like an adviser rather than a spectator.

Preparing yours

Source from primary documents, not summaries: the announcement press release for the terms, the investor presentation for the rationale, the target's last annual report for the operating numbers. Thirty minutes across those three gives you facts nobody can dispute and the vocabulary the deal team itself used, and it protects you from inheriting someone else's error, which an interviewer who worked the deal will spot instantly.

Build a one-page sheet per deal in the five-part shape, say it aloud until the headline and terms are automatic, and prepare the three questions you would ask if you were the interviewer. Sector interviews raise the bar on rationale: if you are interviewing with a technology group, the metrics that matter are different, and I have covered what TMT interviews actually ask separately. Final rounds will run this exact exercise under pressure alongside everything else, which is why it features in my piece on how superdays and assessment centres are scored.

FAQ

Does my deal need to involve the bank I am interviewing with?

No, but knowing one of their recent deals is cheap insurance, because some interviewers ask for exactly that. Prepare one house deal at headline-and-rationale depth and one market deal at full depth.

How many numbers should I memorise?

Five to seven per deal: size, price, premium, one or two operating figures, dates. Enough to prove rigour, few enough to stay accurate under stress. Precision on a handful beats vagueness across dozens.

What if the interviewer knows the deal better than I do?

Expect it, and treat it as an opening rather than a threat. Give your structured view, then ask what the inside version looked like. Interviewers enjoy correcting a good answer far more than rescuing a bad one.

If you want your deal answer stress-tested by someone who sat on the other side of the table for fifteen years, the IBD Recruiting Review does exactly that, live, with the follow-ups included.

Book the 60-min IBD ReviewView Full Cycle

Former Executive Director in TMT Investment Banking at Nomura and M&A banker at BNP Paribas. Top-rated Head Mentor on Wall Street Oasis with 300+ sessions. About